The question that many investors appear to be asking themselves right now is if we will see a recession – prompted by concerns that higher interest rates will undermine economic growth.

I do not know if there will be a recession in the world’s major economies this year or next, and our approach to investing is not based on trying to second guess this. What I do know is that there have always been periods of economic contraction in history. I think of it like waiting at a bus stop with no timetable – you may have absolutely no idea when the next bus will arrive, but you shouldn’t be surprised when one does appear.

For the companies that we follow I take a casual interest in broker research and, of late, I have seen many “target prices” revised down by amounts as large as 25% or more. One way, or another, these revisions are blamed on the fear of a recession causing lower earnings. I struggle to see the justification for such large changes, as surely any reasonable judgement of valuation would look far enough into the future to anticipate one or two bad years.

Moving on from bus-stop analogies, the noise of financial punditry reminds me of the sirens from Greek mythology, who lured sailors to their death with their alluring songs. The mythical Greek hero Odysseus avoided this fate by strapping himself to the mast of his boat and plugging his sailors’ ears with beeswax. I wouldn’t advocate going this far to ignore the financial news, but I do think that it requires determination not to get drawn into the short-term narrative of markets. We certainly want to be alert to changes in our environment, but do not believe that success will come from trying to make timing calls about a recession.

What were we thinking?

So far this year the performance of the fund has been helped by two distinct views that I have previously written about. I thought it was worth recapping them.

In my first quarter 2021 investor letter I wrote about our growing concern that the amount of money that central banks and governments were injecting into their economies would cause higher inflation.

While we do not make investment decisions based on macro-economic forecasts, we do want to own a portfolio that will be robust to perceived threats. In this case we made efforts to consider the impact of higher levels of inflation on our holdings, and those companies engaged in the primary production of energy, food and gold have “held up” as we had hoped, as the threat became a reality.

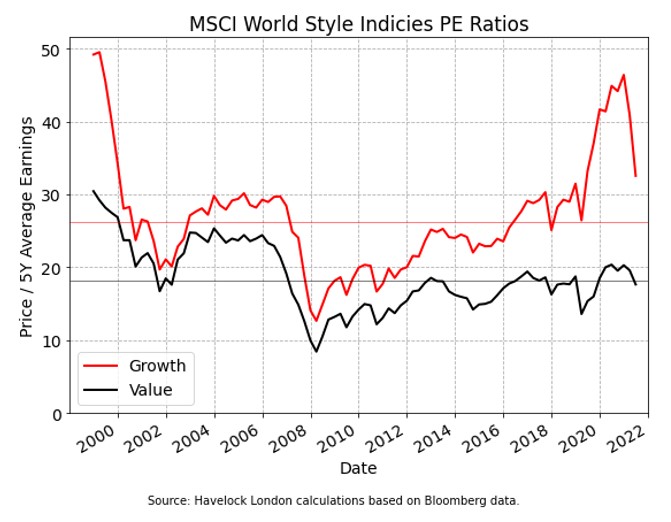

In my year end 2020 letter I set out the case for financial markets being in a bubble, having shared our analysis in my Q3 2020 letter on the evidence for much of the outperformance of “growth” over “value” being driven by price earnings multiple expansion.

There have been two distinct types of “growth” company that investors have been pursuing. The first are companies, with no profits, where the value placed on them is based on a belief about the distant future. The second being companies that are highly profitable, but where investors have paid ever higher premiums to own them. In broad terms both types of growth company have seen price falls this year, with the former being impacted more than the latter. Our valuation driven approach has helped us avoid the worst of this excess.

Before I start to sound too clever, we know full well that our abilities as investors can only reasonably be judged based on our long-term track record. Nonetheless it is gratifying to feel that our analytical investment views have been shown to have merit.

Matthew Beddall, CEO and Fund Manager