As an active investment manager, we put ourselves forward as being able to deliver better than average performance for our clients. This is a tall order. To believe it is possible requires either hubris or a belief that we have an edge over other investors.

Setting out to manage other people’s money based on excessive self-confidence alone is not a great plan. Despite this, the investment industry can often encourage such behaviour. In the short-term you can get lucky, whereas it takes years to demonstrate true skill. Narratives are often crafted retrospectively, which can draw both investment manager and client into a belief that everything the former touches turns to gold.

Real investors understand the importance of remaining humble.

So, what then, do I think is our edge? I see three distinct sources, one that is transient and two that are permanent.

A Value Investing Tail Wind

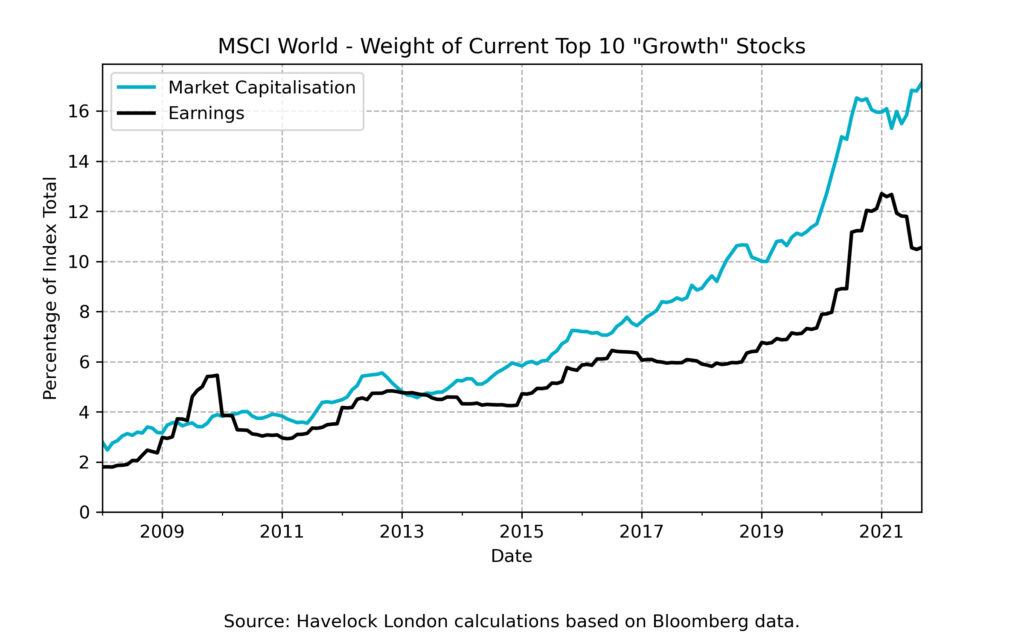

The “growth” style of investing has had a prolonged period of outperforming “value”, such that there are many more proponents of the former than the latter. As I have written about before, the evidence suggests that this out-performance was driven much more by the price investors are willing to pay to own a high growth company than by actual growth in earnings.

In the long run we believe that the returns from owning a company will mirror the underlying earnings from their business and I think many investors are proceeding in the belief that this is not so.

Relative to history the optimism pessimism “gap” between “growth” and “value” styles looks extreme (as measured by the price-earnings multiples of indices on the two cohorts). As a value investor I believe this means we are fishing in a pond with less future success “baked” into the share price of companies at a moment in time when there is less competition to land these catches. It is this that I think could provide us with a transient edge.

Time horizon

If you can think like a long-term investor, I believe it conveys an advantage. It is however easier said than done.

One of the companies that we are a part owner of recently experienced a bump in the road. The company shut down a new initiative, at great expense and much embarrassment, because they believed it would never deliver an acceptable return. The company’s share price fell in response to this news, as many investors decided to walk away.

A recent broker research note on the company shared their latest valuation, with a base-case of £26 per share and an optimistic-case of £33. At the time the note was written the share price was around £19. With a potential 30% upside, you would have thought the brokerage house would be tripping over themselves to recommend buying the shares. However, their outlook was “neutral” because the “path and timing of the potential value crystallization remains unclear”.

This story is typical of the unhealthy focus on the short-term that I see in markets. In the case of this company we may, or may not, be right and we certainly do not know what the catalyst for a share price increase will be. What I do believe is that attempting to “time” a purchase or sales based on second guessing what the short-term will hold leads you down a path of missed opportunity. Being a long-term investor requires patience, often in the face of discomfort, which is a virtue I do not see being widely practiced.

Ignoring the noise

We live in an age where we receive a virtual firehose of information on a 24/7 basis. This leads to the stereotype of the investment professional sat in front of banks of screens full of scrolling news and flashing numbers. As you get drawn into this world, the nuggets of information give our brains little dopamine hits and draw you into thinking they have an exaggerated importance.

My formal training (many years ago) was in statistics. This taught me the importance of looking beyond the noise that we are confronted with in so many aspects of life. I see this skill as related to, but distinct from, being a long-term investor. All investors have limited bandwidth – which means that time is your most valuable commodity. Even a long-term investor can squander their time with distractions that are ultimately not important.

When we make an investment decision, it is based on a thesis, which sets out why we think it will be successful. In my opinion a good investment thesis normally depends on one or two “big” things, rather than many “small” ones – being able to see the “wood for the trees”. I think that the human brain is wired to be distracted by “noise”, and if you can overcome this it will help to make better investment decisions.

Alignment of interest

My savings are invested in our fund, which provides an alignment of interest with our customers that seems surprisingly rare in an industry where you are not expected to eat your own cooking. Furthermore, Neil and I are owner-operators of our business, which I think means that our decisions are less clouded by career risk than is often the case.

I believe that being a large investor in the fund, and part-owner of the management company, helps reinforce the edges that I describe above. I believe it makes me more able to focus on long term investment decisions and less distracted by short-term noise.

I do not know the extent to which these advantages will help us deliver on our goal of delivering good long term compound returns. What I hope you are reassured by is that we are not proceeding based on hubris. In the land of the blind, the one-eyed man is king!